The Essential Advice for Property Investors

Continuously inhabited for over 2,000 years, Leicester truly is the beating heart of England. It’s a unique Bricks and mortar: Buy-to-let is a popular option for those who would rather grow their wealth through property than shares or cash

For many buy-to-let looks an attractive income investment at a time of low rates and stockmarket volatility. But if you are considering investing in property – or improving your returns on a buy-to-let you already own – it’s important to do things right. Read these top ten buy-to-let tips – the essential guide to successful property investing.

Buy-to-let may not be quite the hot property of the boom years, but it has seen a resurgence in recent times.

As an income investment for those with enough money to raise a big deposit buy-to-let looks attractive, especially compared to low savings rates and stock market volatility.

Meanwhile, the property market bouncing back has encouraged more investors to snap up property in the hope of its value rising.

Mortgage rates at record lows are helping buy-to-let investors make deals stack up – you could fix a mortgage for five years at just over 3 per cent at the biggest deposit level.

But beware low rates. One day they must rise and you need to know your investment can stand that test.

Recent history provides an important lesson in that. Many investors who bought in the boom years before 2007 struggled as mortgage rates rose. A sizeable number were thrown a lifeline when the base rate was slashed to 0.5 per cent.

Rates have stuck there since 2008, but remember they will rise again.

Despite the potential for costs to rise, more tenants in the market, rising rents and improving mortgage deals have tempted investors once more.

If you are planning on investing, or just want to know more, we tell you the ten essential things to consider for a successful buy-to-let investment.

Like any investment, buy-to-let comes with no guarantees, but for those who have more faith in bricks and mortar than stocks and shares below are This is Money’s top ten tips.

Buy-to-let Mortgage Rates Tumble, But Beware The Big Fees

Buy-to-let rates have followed residential deals down, but remain slightly more expensive than mortgages offered to owner occupiers.

Landlords need to beware fees, which can substantially push up the cost of a mortgage, especially if they are only fixing or tracking for a short deal period.

The biggest fees are typically those charged as a percentage of the loan but even flat fees can run to £2,000. The good news is that you should be able to claim these back against tax, speak to an accountant if you need help with this.

Natwest offers the lowest fixed rate buy-to-let mortgage on the market at 2.25 per cent with a £1,995 fee, but you will need to have 40 per cent to put down.

A slightly higher two-year fixed rate for landlords is 2.34 per cent from Virgin Money, this requires a £1,995 fee but comes with £500 cashback.

For a longer term five-year deal, Abbey for Intermediaries has a rate of 3.29 per cent with a £1,500 fee. A slightly higher five-year fix is also from Virgin Money at 3.19 per cent. It also has a £1,995 fee and £500 cashback.

Both these loans require a 40 per cent deposit.Typically buy-to-let borrowers must put down a deposit of at least 25 per cent. The best two year fix at this level is from Abbey for Intermediaries with a two-year fixed rate at 2.79 per cent with a £1,995 fee for a 25 per cent deposit.

You could fix for five years with Metro Bankat 3.79 per cent with a £1,999 fee.

1. Research the market

If you are new to buy-to-let, what do you know about the market? Do you know the risks, as well as the benefits.

Make sure buy-to-let is the investment you want. Your money might be able to perform better elsewhere.

In recent years a high-rate savings account would beat most investments. Now rates are lower, but investing in buy-to-let means tying up capital in a property that may fall in value.

This compares to the possibility of a 5% annual return from an income-based investment fund, or 3 per cent on a fixed rate savings account.

Remember that the return from an investment in funds, shares or an investment trust through an Isa will see you escape tax on income and get capital growth tax free. You will also have the ability to sell up quickly if you want.

The flip-side is that you cannot buy an unloved investment fund and set about renovating it and adding value yourself.

Investing in buy-to-let involves committing tens of thousands of pounds to a property and typically taking out a mortgage. When house prices rise, this means it is possible to make big leveraged gains above your mortgage debt, but when they fall your deposit gets hit and the mortgage stays the same.

Property investing has paid off handsomely for many people, both in terms of income and capital gains but it is essential that you go into it with your eyes wide open, acknowledging the potential advantages and disadvantages.

If you know someone who has invested in buy-to-let or let a property before, ask them about their experiences – warts and all.

The more knowledge you have and the more research you do, the better the chance of your investment paying off.

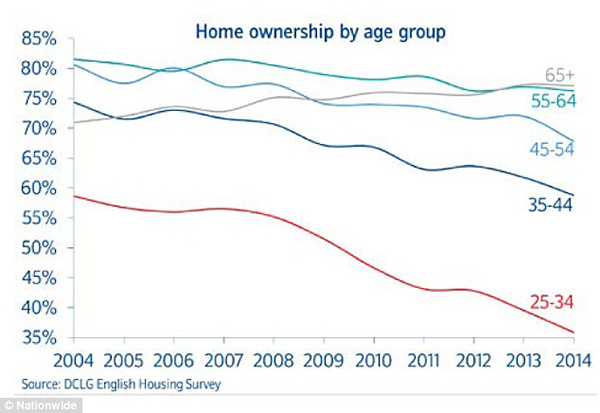

Rising demand: Levels of home ownership are falling, particularly among young people, meaning more renters

2. Choose a promising area

Promising does not mean most expensive or cheapest. Promising means a place where people would like to live and this can be for a variety of reasons.

Where in your town has a special appeal? If you are in a commuter belt, where has good transport? Where are the good schools for young families? Where do the students want to live?

You need to match the kind of property you can afford and want to buy with locations that people who would want to live in those homes would choose.

These questions might sound overly simplistic, but they are probably the most important aspect of a successful buy-to-let investment

In most cases people tend to invest in property close to where they live. On the plus side, they are likely to know this market better than anywhere else and can spot the kind of property and location that will do well. They also have a much better chance of keeping tabs on the property.

Yet it is also worth bearing in mind that if you are a homeowner then you are already exposed to property where you live – and looking for a different type of home in a different area might be a good move.

3. Do the maths

Before you think about looking around properties sit down with a pen and paper and write down the cost of houses you are looking at and the rent you are likely to get.

Buy-to-let lenders typically want rent to cover 125% of the mortgage repayments and many now demanding 25% deposits, or even larger, for rates considerably above residential mortgage deals.

The best rate buy-to-let mortgages also come with large arrangement fees.

Once you have the mortgage rate and likely rent sorted then you must be clinical in deciding whether your investment work out?

Don’t forget to factor in maintenance costs.

What will happen if the property sits empty for a month or two?

These are all things to consider. Make sure you know how much the mortgage repayments will be and if it is a tracker allow for rates to rise.

4. Shop around and get the best mortgage

Do not just walk into your bank and building society and ask for a mortgage. It sounds obvious, but people who do this when they need a financial product are one of the reasons why banks make billions in profit.

Read This is Money’s buy-to-let section for details of latest buy-to-let mortgage deals highlighted and check lenders’ websites, Skipton BS, BM Solutions, NatWest, Woolwich, Coventry BS, Platform (part of Co-op Bank) and Accord (part of Yorkshire BS) have been consistent in recent years.

It pays to speak to a good independent broker when looking for a buy-to-let mortgage. They can not only talk you through what deals are available but they can also help you weigh up which one is right for you and whether to fix or track.

You should still do your own research though, so that you can go into the conversation armed with the knowledge of what sort of mortgages you should be offered.

Can You Still Get Into Buy-to-let?

Many long-term existing buy-to-let investors are sitting comfortably on low mortgage rates, having seen standard variable rates fall as base rate was slashed down to 0.5%.

Some buy-to-let deals before the financial crisis did not have typical SVRs but a revert rate that tracks the bank rate. Long-term landlords are benefiting from that still.

However, new buy-to-let mortgage deals remain more expensive than residential deals and require a big deposit.

If investors are willing to accept that they may find the value of their property slides in the short term, and can ensure their property meets the criteria of 75% loan-to-value and returning 125% of monthly mortgage payments then it can be a good long-term investment.

The key is to think long-term though.

5. Think about your target tenant

Instead of imagining whether you would like to live in your investment property, put yourself in the shoes of your target tenant.

Who are they and what do they want? If they are students, it needs to be easy to clean and comfortable but not luxurious.

If they are young professionals it should be modern and stylish but not overbearing.

If it is a family they will have plenty of their own belongings and need a blank canvas.

Remember that allowing tenants to make their mark on a property, such as by decorating, or adding pictures, or you taking out unwanted furniture makes it feel more like home.

These tenants will stay for longer, which is great news for a landlord.

It is also possible to take out an insurance policy against your tenant failing to pay the rent, usually known as rent guarantee insurance. This can cost as little as £50, and is available as a standalone product from a specialist provider, or as part of a wider landlord insurance policy.

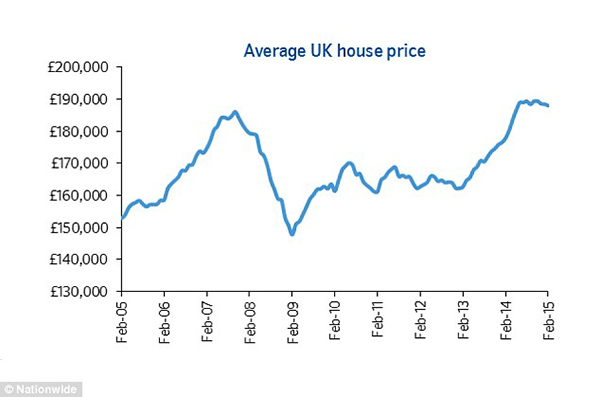

Starting to sink? When compared on a month-by-month basis prices are actually falling, Nationwide found

6. Don’t be over ambitious – go for rental yield and remember costs

We have all read the stories about buy-to-let millionaires and their huge portfolios.

But while you may expect long-term house price rises, experts say invest for income not short-term capital growth.

To compare different property’s values use their yield: that is annual rent received as a percentage of the purchase price.

For example, a property delivering £10,000 worth of rent that costs £200,000 has a 5% yield.

Rent should be the key return for buy-to-let.

How To Work Out The Return On Your Investment

Remember, if you are buying with a mortgage, rent-to-property price yield will not be the return you get.

To work out your annual return on investment subtract your annual mortgage cost from your annual rent and then work this sum out as a percentage of the deposit you put down.

For a £100,000 property that could rent for £500 per month, you would need a £25k deposit and roughly £2,000 in buying costs.

£75k mortgage at 5% interest rate = £312.50

£500 rental income x 12 = £6,000

Difference = £2,250

Deposit + buying costs = £27k

Annual return = 8.3%

Don’t forget tax, maintenance costs and other landlord expenses will eat into that return.

Most buy-to-let mortgages are done on an interest-only basis, so the amount borrowed will not be paid off over time.

This is tax efficient, as you can offset mortgage payments against your tax bill.

If you can get a rental return substantially over the mortgage payments, then once you have built up a good emergency fund, you can start saving or investing any extra cash.

Remember though, people rarely buy a home outright and they come with running costs, so mortgage costs, maintenance and agents fees must be worked out and they will eat into your return.

You may want to consider whether buy-to-let still beats an investment fund or trust once these costs are taken into account.

Once mortgage, costs and tax are considered, you will want the rent to build up over time and then potentially be able to use it as a deposit for further investments, or to pay off the mortgage at the end of its term.

This means you will have benefited from the income from rent, paid off the mortgage and hold the property’s full capital value.

7. Consider looking further afield or doing a property up

Most buy-to-let investors look for properties near where they live.

But your town may not be the best investment.

The advantage of a property close by is being able to keep an eye on it, but if you will be employing an agent anyway they should do that for you.

Cast your net wider and look at towns with good commuting links, that are popular with familes or have a sizeable university.

It is also worth looking at properties that need improvement as a way of boosting the value of your investment. Tired properties or those in need of renovation can be negotiated hard on to get at a better price and then spruced up to add value.

This is one way that it is still possible to see a solid and swift return on your capital invested. If you can add some value to a home straight away then it gives you a greater margin of safety on your investment

However, remember to ensure that the price is low enough to cover refurbishment and some profit and that you allow for the inevitable over-run on costs.

A good rule to follow is the property developers’ rough calculation, whereby you want the final value of a refurbished property to be at least the purchase price, plus cost of work, plus 20 per cent.

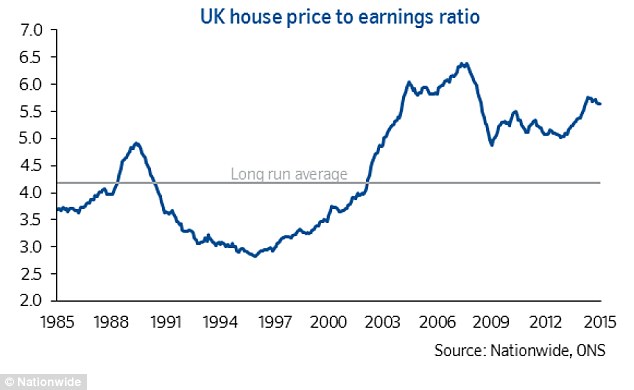

Pricey: On Nationwide’s measure which uses average earnings across the board, property is far more expensive than it was at the end of the 1980s boom – this is driving more people to rent, but may also limit capital gains on property

8. Haggle over price

As a buy-to-let investor you have the same advantage as a first-time buyer when it comes to negotiating a discount.

If you are not reliant on selling a property to buy another, then you are not part of a chain and represent less of a risk of a sale falling through.

This can be a major asset when negotiating a discount. Make low offers and do not get talked into overpaying.

It pays to know your market when negotiating. For example, if the market is softer and homes are taking longer to sell you will be better able to negotiate. It is also useful to find out why someone is selling and how long they have owned the property.

An existing landlord who has owned a property for a long time – and is cashing in their capital gains -may be more willing to accept a lower offer for a quick sale than a family that needs the best possible price in order to afford a move.

9. Know the pitfalls

Before you make any investment you should always investigate the negative aspects as well as the positive.

House prices are on the up right now but growth has slowed and they could fall again. If property prices dip will you be able to continue holding your investment?

Meanwhile, rates are low at the moment and that is encouraging people to invest with rent comfortable covering the mortgage, but what will you do when rates rise?

Consider too the standard variable rate you may move to after a fixed rate period. What will happen if you can’t remortgage?

Even in popular areas properties can sit empty. One rule of thumb many buy-to-let investors apply is to factor in the property sitting empty for two months of the year – this gives a substantial buffer.

Homes often need repairing and things can go wrong. If you do not have enough in the bank to cover a major repair to your property, such as a new boiler, do not invest yet.

10. Consider how hands-on you want to be

Buying a property is only the first step. Will you rent it out yourself or get an agent to do so.

Agents will charge you a management fee, but will deal with any problems and have a good network of plumbers, electricians and other workers if things go wrong.

You can make more money by renting the property out yourself but be prepared to give up weekends and evenings on viewings, advertising and repairs.

If you choose an agent you do not have to go for a High Street presence, many independent agents offer an excellent and personal service.

Select a shortlist of agents big and small and ask them what they can offer you.

If you are considering going it alone look at where you will advertise your property and where you will get documents, such as tenancy agreements from.

It really pays to look after your tenants. Do this and they will look after you.

The biggest drag on many buy-to-let landlord’s investment returns is the void period. A time when you don’t have anyone in the property. Good tenants who want to stay help avoid this – and if they move on they may even recommend your property to someone they know.

Keep up with maintenance, make sure your property is a nice place to live and try and build a good personal relationship with your tenants.

Original Article By Simon Lambert for Thisismoney.co.uk Updated: 08:34, 22 April 2015

Bloom Towers | Dubai

Bloom Towers | Dubai Park Lane | Dubai

Park Lane | Dubai Jumeirah Luxury | Dubai

Jumeirah Luxury | Dubai Azizi Riviera | Dubai

Azizi Riviera | Dubai Bloom Heights | Dubai

Bloom Heights | Dubai